ChatGPT, Claude, or Gemini? Big Pharma Is Choosing Sides

I tracked 27 frontier-AI partnerships across 21 pharma companies. Here’s what the map looks like and what it means.

Every industry is trying to get smart on AI, and BioPharma is no different.

Over the course of this year we have seen a slew of press releases outlining major partnerships between our sector’s major players and a cornucopia of AI-houses. These range all the way from tiny companies that are using AI to model biology and speed up drug discovery all the way up to the so called “frontier labs”.

This “frontier labs” group is what I wanted to focus on for this post. ChatGPT, Claude, and Google Gemini are probably the three most popular large language models (LLMs) the average person interacts with (sorry Grok 😢).

You probably use one of these to figure out recipes based on a picture of what is in your fridge, draft a polite email to an annoying vendor that keeps bugging you about how they can “bring you 5-10 new leads per week”, or to settle dumb debates with your partner, like whether the dishwasher actually requires pre-rinsing (it doesn’t…just buy better detergent) or if peanut butter should be stored in the fridge (that is overkill…plus it makes it way harder to spread and life is difficult enough).

Your favorite Big Pharma company is using one or two of these frontier models as well, but only for more complicated things.

AI is making its way into BioPharma one way or another. It’s here to stay. As I noted in a previous post, these Tech/AI companies are quickly running out of room to innovate in the realm of software. LLMs are based off of code and are really great at doing things that require coding, like developing software. They are built on code and understand code super well. Eventually massive swaths of that space are going to get commoditized, leaving AI to need to find greener pastures to graze. There is no greener pasture than advancing human health via novel therapeutics.

Given these AI companies are pervasive across our daily life and are going to be IPO’ing soon(ish) with massive valuations to give them even more momentum to make inroads with BioPharma, I wanted to take a look at who is partnering with who and for what purposes. What trends can we see? What insights can we glean, when we look at how Big BioPharma and Big AI are coupling up?

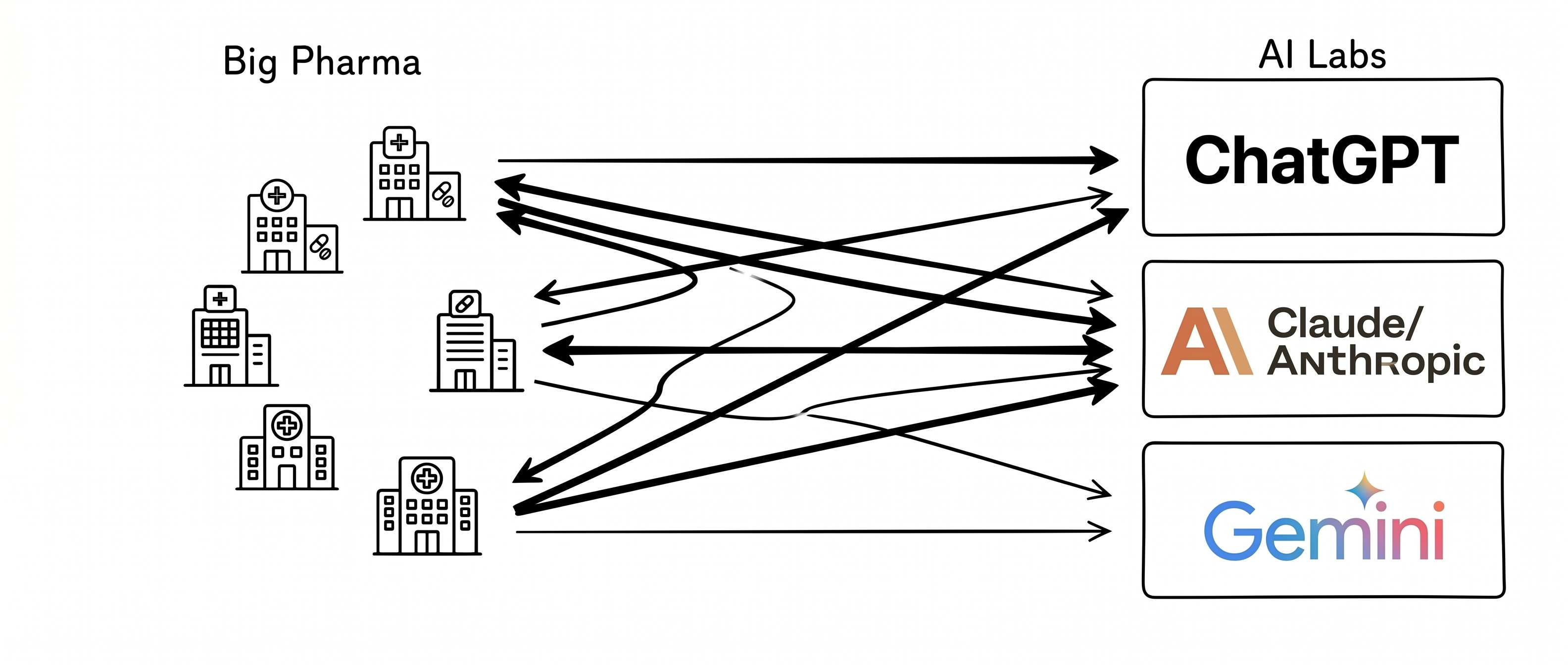

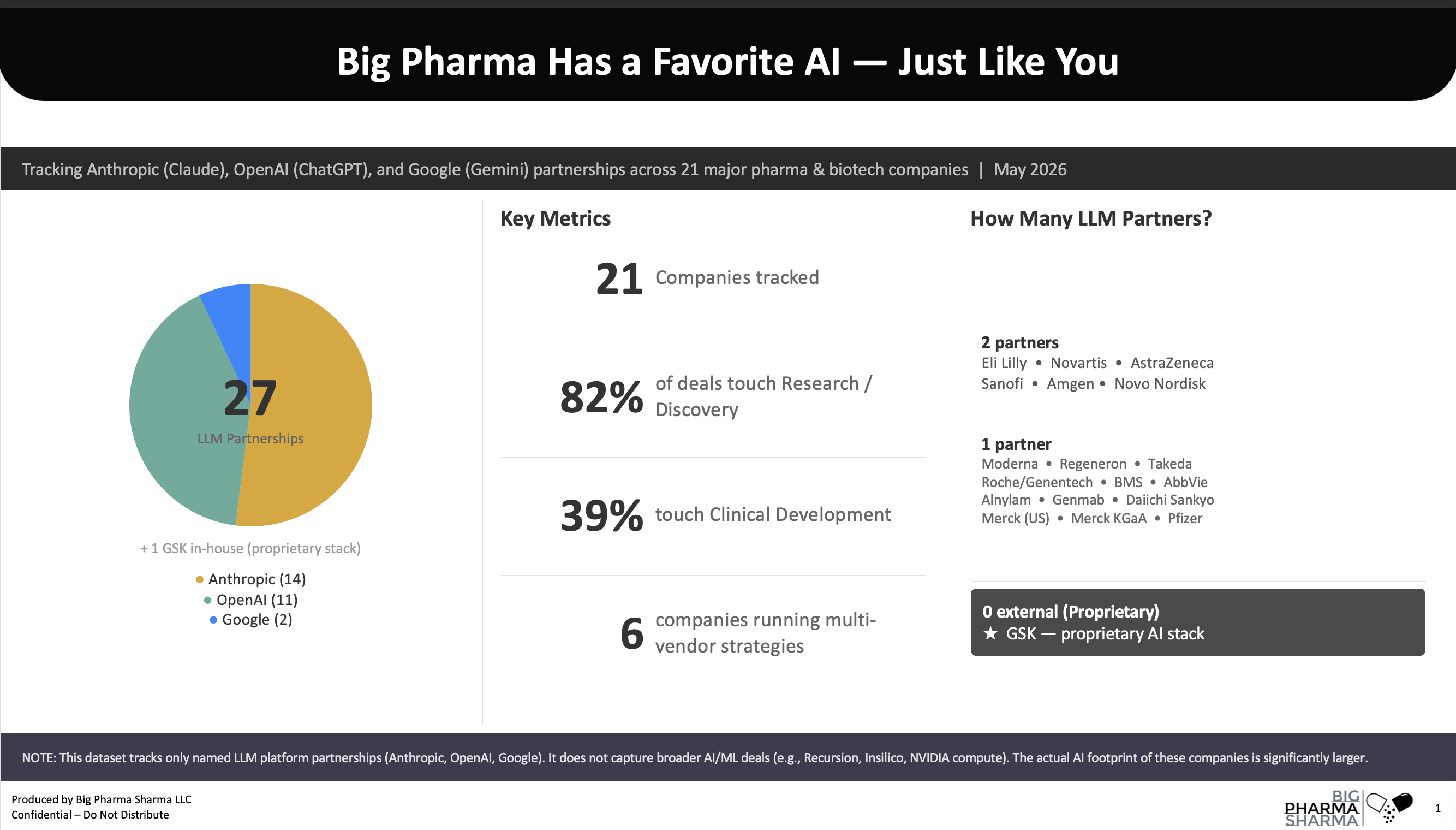

As of May 2026, I've tracked 27 confirmed strategic partnerships between frontier LLM providers and major Pharma companies, plus one company (GSK GSK 0.00%↑ , more on them later) that has decided to build the whole thing in-house and tell the AI labs to kick rocks.

This dataset only tracks named partnerships with Anthropic, OpenAI, and Google Gemini. It does not include the broader AI footprint in our sector, which is massive. Recursion, InSilico, AbSci, NVIDIA NVDA 0.00%↑ compute deals, the various academic collaborations, and the dozens of internal data science teams running their own thing are all excluded unless they show up in a named LLM contract.

The actual AI surface area inside Pharma is much bigger than 27 deals. The focus of this exercise is to zero-in on the frontier AI models and how they are being used by the big companies.

The AI + Big Pharma Collaboration Landscape

If you’re a free subscriber, you are probably receiving my Last Week Tonight in Biopharma weekly series. If my opinions and insights there have helped you, please consider becoming a paid subscriber to read this full post (with slides and downloadable full database) and get all my other work.

Most of the top companies are using Anthropic/Claude in one way or another, with 52% share of the 27 deals I was able to find evidence of. Open AI is second with 11 deals (41%) and Google Gemini with just two deals, but notably one of them is with Merck MRK 0.00%↑ with the largest disclosed value of $1B.

Six companies are not tying their fates to one horse, and are partnered with both OpenAI and Anthropic.

Only GSK sits alone, with no external LLM partnerships that I could find. Instead they seem to be building their own, called JulesOS, with the help of their own AI/ML engineers. I found this zag from GSK quite interesting. In their view, they see the advantage of build (vs. buy) as as mitigating clinical-risk hallucinations, safeguarding multi-billion dollar pre-clinical IP, and unlocking proprietary functional genomics datasets that public LLMs cannot access. We will see how this shakes out over time, but the fact that GSK built their own, while their competitors are working with the leading players, allows GSK to serve as somewhat of an active control group.

The functional distribution tells you where the field thinks LLMs actually work today. Unsurprisingly, 82 percent of these deals touch Research and Discovery in some form and then Clinical Development as the next most common functional area. I would have expected manufacturing/CMC to be more common, but there are only a handful of these partnerships that have disclosed manufacturing implementations.