Big Pharma at JPM 2026: M&A, Obesity, and China

How patent cliffs are dividing Big Pharma's M&A approach, plus obesity market battles, direct-to-consumer shifts, and China's innovation role

JPM is always a tone-setter for the year in BioPharma. Everybody tunes into what the biggest companies in our space have to say. What’s their M&A appetite? How are they thinking about China? What about Trump? Platforms or Products? Their commentary dictates how other parts of our sector view their own businesses.

At some level, our sector is the truest expression of 'trickle-down economics.' When Big Pharma decides to buy or partner, that capital recycles back into VCs and public investors, eventually funding the next generation of Series A startups. More M&A at the top means bigger and more exits, and may in turn influence a functional IPO window and a reason for early-stage investors to keep writing checks.

So every year what is said during this week is important, even if it feels like there are less and less people hovering around San Francisco during this time of the year. The streets are less lively. The random bump-ins are less frequent. The after-parties have more elbow-room. Still the tone is set from the top - and that’s what today’s post is all about.

I dug through transcripts and slides from all the Big Biopharma companies1, connected the dots, and pulled out several key themes, insights, and implications that portend to shape the year ahead. Let’s get into it.

M&A Philosophy Divide

If you enjoy strategic analyses, insights, and opinions about the Biotech and Pharma from an insider’s perspective, you can get access to all Big Pharma Sharma content becoming a paid subscriber. Thanks for your support!

Often times you hear a lot of the same talking points on key topics across the Big Biopharma CEOs. M&A can sometimes fall into this category. “We’re interested in bolt-on deals”. “We have an appetite for late-stage de-risked assets”. “We like pipeline-in-a-product type deals with clinically de-risked programs”. Certainly we’ve heard all that before and heard versions of that even at this JPM.

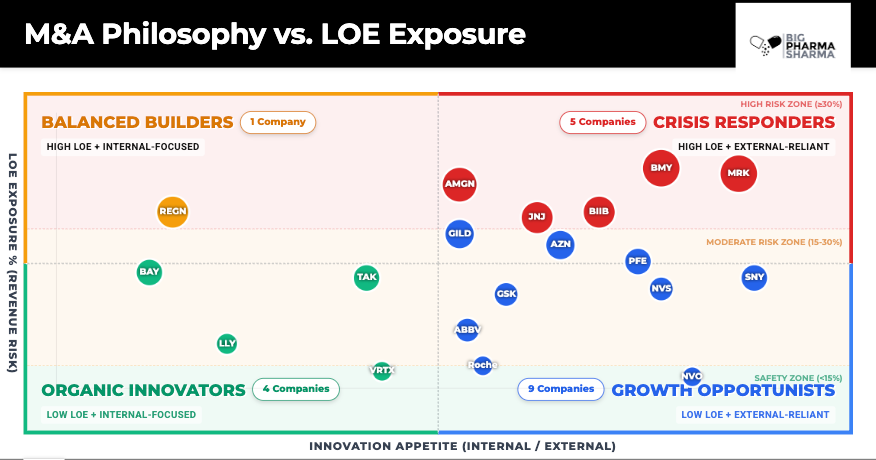

The real striking divide this time around was M&A philosophy. The matrix I created above is a helpful framing for where each major players sees themselves with regards to their desire to do deals and their LOE exposure (% of 2025 revenues facing erosion in the next 5 years).

Most companies sit in the bottom right quadrant, called “Growth Opportunists”. They have relatively moderate to low LOE exposure over the next five years, strong balance sheets, and are able to do deals more selectively with less pressing need for large late-stage acquisitions that bring in near-term revenues. They can jump into big meaty transactions if they want to, but it’s not as pertinent. It’s perhaps surprising to see a company like AbbVie and Roche in this quadrant, however both companies are largely past their major patent cliffs, digesting previously large acquisitions or big partnerships, and cultivating those programs now in-house.

The more interesting groups sit in the other three quadrants though.

In the top right you have companies (I am calling ‘Crisis Responders’) who have the highest percentage of their revenues threatened by patent cliffs and have naturally been the most acquisitive, and would seem to continue to be given their JPM commentary. BMS and Merck aiming to fill the forthcoming PD-1 revenue gaps with their slurry of late stage acquisitions are great examples of an aggressive external innovation strategy. Others in this group, like J&J and Amgen who do have rather significant revenues at risk over the next five years, appeared more balanced in their internal/external innovation split, and are more focused on early stage deals (per their comments) with optionality for larger deals if the right one comes up. Still, in those cases, deals to build the pipeline will likely play a roel

In contrast to this group sits Regeneron, a lone ranger of sorts. Its commercial revenues are at a relatively high (~30%) LOE risk, but their management made it a point to take a contrarian position against large-scale M&A, arguing that such deals lead to “value destruction”. Instead, Regeneron is betting on themselves, focusing 95% of its R&D resources on internal programs to organically grow out of oncoming patent cliffs and formulation strategies like transitioning its retina franchise from EYLEA to EYLEA HD to mitigate biosimilar erosion (note: it appears they are looking to take forward a similar strategy to stave off DUPIXENT patent cliffs in 2030).

As a strategy guy, I love that Regeneron came into JPM with such conviction on their plan. It shows a deep evaluation both of their own company strengths (which has long been their proprietary genetic and antibody platforms) and performance of their peers’ strategies. Regeneron is uniquely equipped to organically grow out of their patent cliffs, because of the strength of their platforms and they know it.

The bottom left, “organic innovators” bucket, is an interesting one too and tells a tale of two stories. On the one hand you have companies like Vertex and Lilly who are well equipped with cash-printing machines (GLP-1s and CF franchise), and have redeployed that capital heavily towards internal R&D but also towards select bolt-on product acquisitions and platform buys that can enhance R&D capabilities. If Regeneron is the home chef that is so good at cooking that eating out would just be a waste of money, Vertex and Lilly are equally talented home chefs, but love a nice fine dining tasting menu every once in a while. Had either of these companies been in the same LOE situation as Regeneron, they probably would also be telling the JPM crowd that they didn’t feel a significant urgency to do big deals, because their R&D engine has had a strong track record of hitting home runs. They could organically grow through their cliffs and pull the trigger on a big deal only if it really made a ton of sense.

On the other hand you have folks like Bayer and Takeda who I think would love to be able to do more deal, but really can’t because they are saddled with debt and/or insufficient firepower. In turn, they are more focused on growing their existing internal portfolios and making the most of what they have now.

An easy takeaway from this chart is that the right half of the slide are going to be your active buyers, bidding each other up and out for the next great product, while the companies on the left will be more or less staying put.