Should You Be Allowed to Bet on Whether a Cancer Drug Works?

My initial view on prediction markets for clinical trials

Earlier this month a new prediction market got a lot of attention on X. It’s called Endpoint Arena. Similar to other prediction markets, like Kalshi and Polymarket, it allows users to place ‘Yes’ or ‘No’ wagers on particular outcomes, only for Endpoint Arena, their menu of markets strictly focuses on clinical trial results. Endpoint Arena specifically appears to be interested in testing whether the frontier AI models can predict clinical trial outcomes, how these models’ prediction abilities compare to one another, and conceivably (from the image below) provide humans an opportunity to make Yes/No bets on the outcomes of specific trials.

The unveiling of this new offering was expectedly divisive, but I think it emerged at the right place and right time for that lightning rod reaction. In fact, the major predictions markets have had similar offerings for a while now. Real-money wagering on drug-related regulatory events is already happening. With Substack’s Polymarket integration, I’ve pulled in a few examples below:

I held my tongue on this topic because I was still trying to figure out how I feel about all this, as it sort of sits at the intersection of two different passions of mine: drug development and sports betting.

I think I have broad definition of what “gambling” or “betting” is. Sports betting, prediction markets, buying/selling stocks, buying/selling options, etc. all fit under gambling to me. You can lose a lot of money doing all of the above, but if you educate yourself on the right strategies to implement, are incredibly data-driven, and know the right healthy risk-threshold for you, you can do quite well. Every decision we make on a daily basis is either an implicit or explicit calculation of risk and probability. I don’t think any of the above forms of betting are that different.

So look, I am not anti-gambling. It is a vice and should be approached with extreme caution and moderation. Some people shouldn’t be sports betting, just like some people shouldn’t be drinking, just like some people shouldn’t be trading stocks, and just like some people shouldn’t be smoking weed. But if you are able to maintain a healthy relationship with these vices, and not letting them imbalance you in deleterious ways - it’s a free country, you do you.

Nor am I anti-markets. When markets function healthily, with transparency, right-sized regulation, competition, and proper enforcement against corruption, they can accelerate innovation and create tremendous value for both business and consumers.

To help me get to the bottom of how I feel about prediction markets for clinical trials, I structured my thinking around a few questions:

What can we learn from how sports betting markets work?

Note: 90%+ of the trading volume on prediction markets is actually from sports. Kalshi and Polymarket are in large part sports betting exchanges. Sports books and sports betting exchanges, have been around a long time and are the best analog we can glean insights from.

How is Material Non-Public Information (MNPI) different in clinical trial markets?

What is the reality of enforcement in these sorts of prediction markets?

Do these markets align with the overall goal of making successively more types and better kinds of drugs that help people who are sick?

Let me explore each one with you.

The Sports Betting Analogy

Prediction markets and sports betting share some structural DNA. Typically with sports betting you are wagering against “The House”. These are betting platforms like FanDuel, DraftKings, Caesars, PrizePicks - pretty much any second or third advertisement you would see when watching a sporting event. Generally these sorts of companies make money by charging a “vig”, also known as a “spread”.

In the above example, you can either bet the Cardinals to win by 7 or more points (e.g. -6.5) or the Saints to win OR lose by less than 7 points (e.g. +6.5). Both wagers have a price of -110. This is just a funky way that sports books display probabilities. It essential means if you bet $110 you profit $100. If you convert this to percentages, the sports book is saying they think there is a 52.4% chance that Cardinals -6.5 line hits and a 52.4% chance the Saints +6.5 line hits. If you’re following along, that adds up to 105%, which doesn’t make any sense. But that right there is the “vig”. The sports book is trying to solicit equal action on both sides of the bet. If they get $110 on the Cardinals and $110 on the Saints, they’ve collected $220. If the Saints side hits, they need to pay out $210 ($110 wager plus a $100 profit) to the people who bet the Saints. That leaves the sports book with a profit of $10 (a vig of ~5%), paid for by the people who took the Cardinals and lost the bet. Make sense? Sports books are constantly adjusting vigs and odds on each market they create to optimize their potential ROI, by balancing the amount of money on both sides of a bet such that no matter what the outcome is, they make a small profit.

Before going further, It’s important to call out the moral dimension here, and how clinical trials are different from sports. Sports are ultimately a game. Nobody’s life depends on whether the Lakers cover the spread against the Rockets. In clinical trials, especially with severe, life-threatening diseases like cancer, whether a drug works or not for people who are sick is essentially life and death. That distinction matters a lot, even before you get to the structural problems as to how potentially easy prediction markets are to manipulate, and how accurate they actually can be at predicting the future.

You may be able to say, for a small oncology-focused biotech company that trades publicly, there are already people shorting that company’s stock. And so they’re betting on the failure of that company’s lead drug and in turn on those patients not to perform well. And to that person, I would say: yeah, that’s fair. But this aspect of betting on the success or failure of a particular clinical trial does feel meaningfully more direct (or at least much closer) to a patient’s life than betting on the health of a corporate entity.

I don’t have a logical argument to tell you that this is the right way to think about it. But to me, ethically, it feels wrong. That’s not an argument I think will sway a proponent of these sorts of prediction markets, so let me try something else.

Prediction markets function a bit differently than sports books. Instead of betting against Kalshi or Polymarket, you are betting against other people on those apps. Individuals more or less get to set their own lines and the app basically pairs you up with someone (or many someones) on the other side of the transaction. It similar to when you buy or sell a stock on E*TRADE. If I buy 100 shares of Eli Lilly stock, I am buying that from one or more people or entities out there on the internet who I’ll never meet. If you are betting $100 on Cardinals, Kalshi and Polymarket software finds people who collectively have $100 on the Saints. In exchange they charge you a small fee (1-3%). The value of your position can then go up or down based as it gets closer to the final outcome. Because you’ve essentially turned your prediction into a stock, you can trade in/out of that position up until the final outcome of the game is known. So for instance if the Cardinals are blowing out the Saints in the third quarter, my position may be worth more than what it was at the start of the game. I might decide to sell my position before the end of the game just to look in a profit and avoid losing my money to an albeit unlikely late-game comeback by the Saints.

These sorts of exchanges are far more fair on the surface, but much harder to make money on, because you are competing against a lot of smart people who are way better at this than the average person. We call these people “sharps”. They’re typically hedge funds, trading firms, and professional bettors. Just sticking to sports, the typical professional sports bettor hits roughly 53–55% of their bets. That’s a slight edge that they compound over time with volume. Most of the time, they have proprietary algorithms and models. Their formulas look at very obscure parts of the game or track very specific sets of data that may give them an edge and may not be underweighted in the public market.

For example, in basketball there were some famous sports bettors who tracked NBA referees’ foul patterns with regard to specific players. This gave them an edge that wasn’t necessarily priced into sports betting lines. Eventually, the sports book gets smart and incorporates these components into their market-making strategies, and the professional sports bettor needs to find a new edge. In certain cases they may have advanced notice on player injuries, lineup news, or any other material information that hasn’t made its way to the public yet (more on this later).

In the sports world, these markets tend to be more accurate, but it requires one main thing: liquidity. The more money that is trading hands within a particular market, the higher confidence you have in the probabilities that that market displays. Thin markets (total value in the hundreds of dollars) are typically noisy and often incorrect. It’s not just the sheer volume of money exchanging hands that makes a market better at predicting the future. It’s really these expert bettors who are driving the probabilities. If the entire market was a bunch of people only betting 25 bucks a bet on a sport they’d never heard of, over time the market would probably not be all that predictive. Sharps are the ones betting the largest sums of money, but also have the strongest predictive value. But like I said before, even the best predictors of the future (in sports) are right at best 55% of the time.

This liquidity piece, as well as the expertise/sharpness piece, is really important when we think about clinical trial markets. In order for these markets to be really good at predicting clinical trial outcomes, they would need to attract large volumes of money, but also a sufficient volume of sophisticated participants, to produce a meaningful outcome. The Science Policy Forum paper (Packin & Rabinovitz, April 2026) makes this exact point: thin liquidity means even small trades can manufacture the appearance of consensus, turning “forecasts” into instruments of influence.

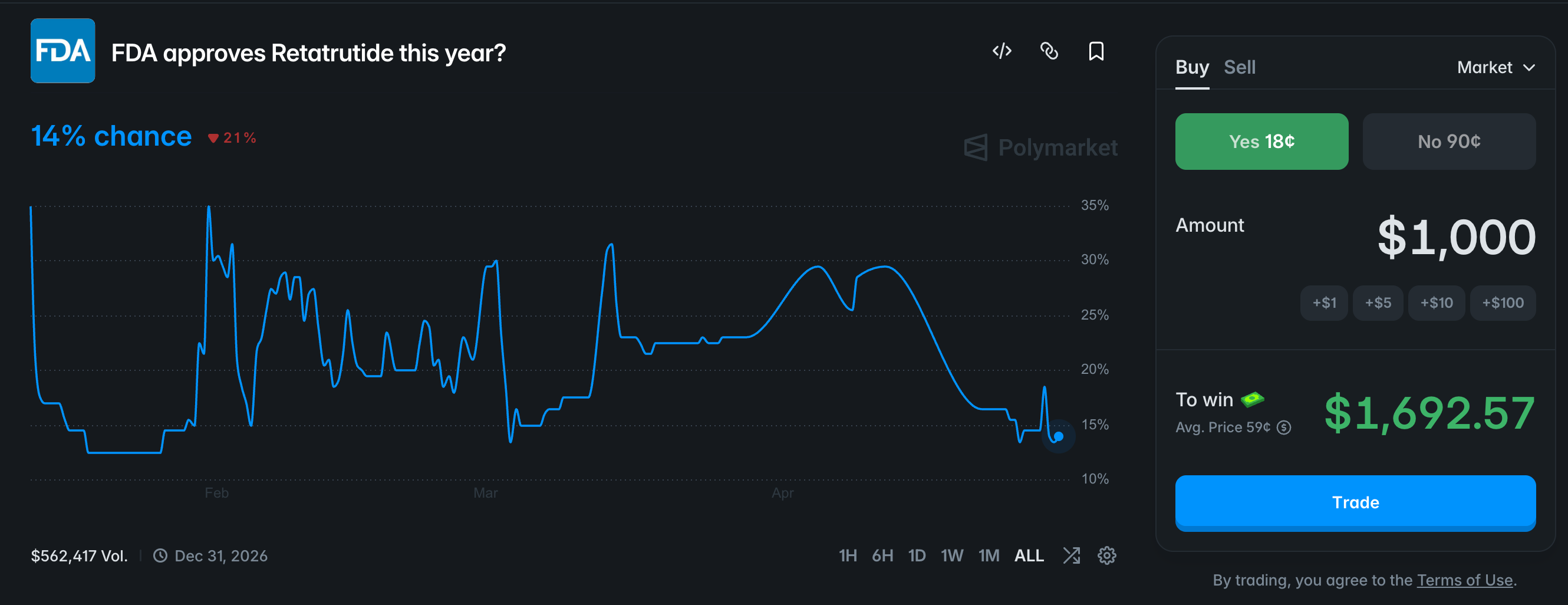

To give you an example of how thin markets can be easily manipulated, let’s take the example I shared earlier about the market for the FDA approving retatrutide this year. If you go to that page on Polymarket, there’s an 18-cent price (aka 18% chance) that the approval happens this year. However, if you bet a relatively small sum of $1,000, the average probability of that event occurring would swing all the way to ~59% (this is where it says “Avg. Price 59-cents”). So just with a $1,000 bet I could move the market here by over 40 points. This tells you that this is a very thin market.